Search by : Pn. Nor Anidah (Penolong Akauntan)

Article by : Lisa Smith

Sumber : https://www.investopedia.com/articles/pf/12/good-debt-bad-debt.asp

Many people believe that having no debt is ideal, but in many situations, debt can actually be considered good for your finances if it helps you build wealth. For example, if you cannot afford to buy a home with cash, you may go into debt with a mortgage. That, in turn, can help you use your housing payments to build a real estate asset instead of renting.

Loans like mortgages are usually considered good debt because they provide value to the borrower by helping them build wealth. However, many other kinds of debt are not as healthy for your finances.

KEY TAKEAWAYS

- Debt can be considered “good” if it has the potential to increase your net worth or significantly enhance your life.

- A mortgage or student loan may be considered good debt, because it can benefit your long-term financial health.

- Bad debt is money borrowed to purchase rapidly depreciating assets or assets for consumption.

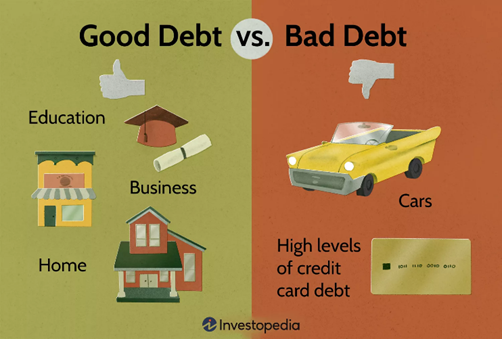

- Bad debt can include high levels of credit card debt, which can hurt your credit score.

- You can manage debt with either a planned budget or debt consolidation.

What Is Good Debt?

If the debt you take on helps you generate income and build your net worth, then that can be considered “good.” So can debt that improves your and your family’s life in other significant ways. Going into debt may be beneficial to your overall financial health in several types of scenarios.

Some expenses that can help you build long-term wealth include:

Education: In general, the more education an individual has, the greater their earning potential. Education also has a positive correlation with the ability to find employment. Better educated workers are more likely to be employed in good-paying jobs and tend to have an easier time finding new ones should the need arise. An investment in a college or technical degree can often pay for itself within a few years of entering the workforce. However, not all degrees are of equal value, so it’s worth considering both the short- and long-term prospects for any field of study that appeals to you.

A business: Money that you borrow to start your own business can also be considered good debt. Like paying for education, starting your own business comes with risks. Many ventures fail, but if your business succeeds, then the debt would be worth it.

Your home: There are a variety of ways to make money in real estate. First, you can take out a mortgage to buy a home, live in it, and then sell it at a profit. In the meantime, you also are building equity and will have the potential for tax breaks that are not available to renters. Residential real estate also can be used to generate income by renting it out.

What Is Bad Debt?

Bad debt is generally considered money you are borrowing to purchase a depreciating asset.

Debt that is not healthy for your finances typically carries a high interest rate. Carrying too much debt can negatively affect your credit score. If you use too much of a revolving line of credit, like charging up to the maximum on your credit card, then your credit score will suffer.2

For example, you may want to avoid debt for:

Cars: You may need to buy a car for transportation, but borrowing money to buy one isn’t a great idea from a financial perspective. As soon as you leave the car lot, the vehicle already will be worth less than the purchase price. If you need to go into debt to buy a car, then look for a loan with low or no interest. You’ll still be investing a large amount of money in a depreciating asset, but at least you can try to save on overall interest costs.

Clothes and consumables: Of course you need clothes—and food, and furniture, and all kinds of other things—but borrowing to buy them by using a high-interest credit card isn’t a good use of debt. Use a credit card for convenience, but make sure you’ll be able to pay off your full balance at the end of the month to avoid interest charges. Otherwise, try to pay cash.

Credit card reward programs give cardholders an extra incentive to spend. But unless you pay your balance in full every month, the interest charges may more than offset the value of your rewards.

Other Types of Debt

Not all debt can be so easily classified as good or bad. It often depends on your own financial situation or other factors. Certain types of debt may be good for some people but bad for others, such as:

Borrowing to pay off debt: For consumers who are already in debt, taking out a debt consolidation loan from a bank or other reputable lender can be beneficial. Debt consolidation loans typically have a lower interest rate than most credit cards, so they allow you to pay off existing debts and save money on future interest payments. The key, however, is making sure that you use the cash to pay off debts and not for other spending. Investopedia publishes regularly updated ratings of the best debt consolidation loans.

Borrowing to invest: If you have an account with a brokerage firm, then you may have access to a margin account, which allows you to borrow money from the brokerage to purchase securities. Buying on margin, as it’s called, can help make you money if the value of the security increases. However, it can cost you money as well if the security loses value. This type of debt is not ideal for inexperienced investors or those who can’t afford to lose money.

How to Manage Debt

If you are carrying debt, you can develop a budget of your income and expenses to help ensure that you can afford all of your monthly payments.

Then, you can work toward identifying which debt you should pay down first and allocate your extra funds toward that debt.

You can also use debt consolidation to help manage debt. With this strategy, you take out a new loan with a lower interest rate to pay off your other loans with a higher interest rate. That way, you can pay down your debt faster and save on overall interest.3

If you cannot afford to pay your debt, you might want to consider debt settlement with your lender or filing for bankruptcy.

What is ‘good debt’?

Borrowing to invest in a small business, education, or real estate is generally considered “good debt,” because you are investing the money you borrow in an asset that will improve your overall financial picture.

What is ‘bad debt’?

High-interest loans, such as those from payday lenders or credit cards, are expensive but can make sense in particular circumstances. A loan is generally considered to be bad debt if you are borrowing to purchase a depreciating asset. In other words, if it won’t go up in value or generate income, then you shouldn’t go into debt to buy it. This includes clothes, cars, and most other consumer goods.

What is debt management?

Debt management is the process of planning your debt liabilities and repayments. You can do this yourself, or use a third-party negotiator (usually called a credit counselor). This person or company works with your lenders to negotiate lower interest rates and combine all your debt payments into one monthly payment.

The Bottom Line

Not all debts are equal. Good debt has the potential to increase your wealth, while bad debt costs you money with high interest on purchases for depreciating assets.

Determining whether a debt is good debt or bad debt sometimes depends on an individual’s financial situation, including how much they can afford to lose. Consider consulting with a professional financial advisor to review your debt situation and your options for managing it.

Date of Input: 22/06/2023 | Updated: 07/04/2026 | muhammad.isam

MEDIA SHARING