Article Search by : Mrs. Nurfarah Hanani Abdul Hamed (Auditor)

Source: https://iiam.com.my/wp-content/uploads/2022/08/e-techline-Issue-4-2022.pdf

The public sector chief audit executive (CAE) is charged with preparing the internal audit activity to respond to increasing challenges and demands for transparency, accountability, and effectiveness at all levels of government and other public sector enterprises. Accomplishing this task may involve establishing a new activity or improving or rejuvenating an existing one that is performing at a less than optimal level.

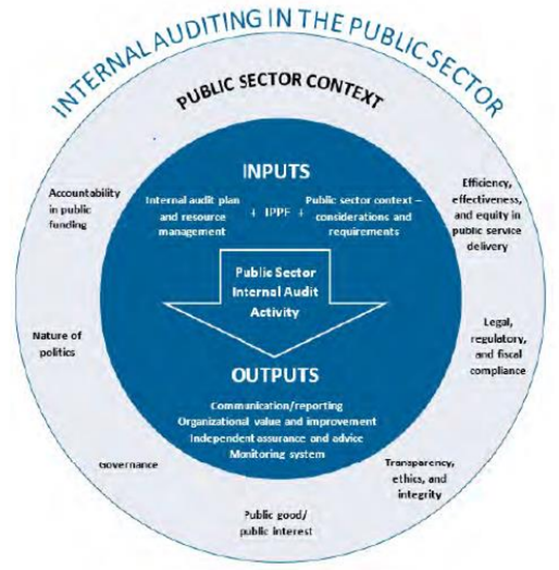

Adding to the demands, the CAE also may be new in the position. As part of their response, the CAE needs to understand the unique aspects of the public sector environment, including threats — political and otherwise — to the internal audit activity’s independence. Internal and external stakeholders, especially the public the organisation serves, rely on the assurances provided by the internal audit activity to ensure that efficient, effective, and equitable use is being made of public funds and the organisation is operating in the public interest. This guidance touches on all seven of the Public Sector Context criteria, or unique aspects of working in the public sector environment, which include:

Accountability in Public Funding

Internal audit must consider effective use of public funds as part of the audit plan and should consider controls in all organisational processes to protect the reliability and integrity of financial information.

Nature of Politics

As part of evaluating culture risk, and to align with the IPPF’s Code of Ethics, the public sector internal audit activity must develop an understanding of political interests.

The results of internal audit work should be disseminated appropriately, even outside the organisation, to improve governance, risk, and control processes, but not for political purposes.

Governance

Internal audit is an integral component of effective governance and helps organisations achieve their objectives and measure their results. If the organisation does not have strong and mature governance processes in place, it may not be adequately prepared for an effective internal audit activity. Internal audit must reflect on and be aligned with the governance of the organisation.

Public Good/ Public Interest

Although typically the internal audit activity does not report directly to the public, all public sector internal audit work should be done on behalf of the public and with the public benefit and interest in mind. The internal audit activity must be assessing what the organisation is doing to provide value to the public.

Transparency, Ethics, and Integrity

Public sector internal auditors must display the highest level of ethics and integrity in their work with the organisation to establish and maintain credibility with internal audit stakeholders, both inside and outside the organisation.

Legal, Regulatory, and Fiscal Compliance

The internal audit activity must become familiar with the laws, rules, and regulations that govern the organisation and consider legal aspects while conducting all assurance and consulting work. Additionally, the internal audit activity must ensure the appropriate governance structure has been established for the activity to ensure it is in compliance with any laws, rules, and regulations affecting internal audit operations within the organisation.

Efficiency, Effectiveness, 2022 and Equity in Public Service Delivery

The ultimate customer of all public sector services is the public. Therefore, public sector internal auditors must consider this important element in planning all assurance and consulting engagements to ensure the results of assurance and consulting work add value to the organisation and ultimately the public. This includes audits focused on government performance and achievement of outcomes.

Date of Input: 30/09/2022 | Updated: 30/09/2022 | nurmiera

MEDIA SHARING